I am continually amazed at the amount of nonsense that I’ve been reading on the subject of moral hazard. Here are a few examples:

1. Moral hazard played no role with SVB because the shareholders and bondholders were wiped out. (nonsense)

2. Moral hazard isn’t an issue because average people don’t think about the safety of a bank when making deposits. (nonsense)

3. Moral hazard isn’t an issue because average people are unable to evaluate the risk of various banks. (wrong)

4. A run on bank deposits could cause a recession. (wrong)

If you see anyone making the first two arguments above, just stop reading. They literally do not know what moral hazard is. The fact that a business failed and the owners lost everything has no bearing on the issue of moral hazard. Here’s Matt Levine:

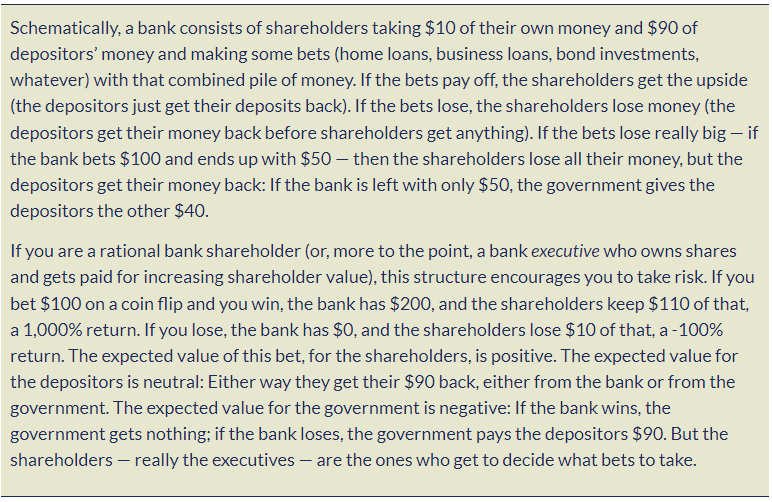

Deposit insurance gives bank executive an incentive to take socially excessive risks. In some cases the risks won’t pay off. But that doesn’t mean executives don’t have an incentive to take excessive risks.

Things didn’t pan out for SVB. But that doesn’t mean their executives made an unwise gamble. It’s very possible that SVB’s strategy had a very high expected payoff, and they were simply hit by bad luck (rising interest rates.) Of course from a social perspective their decisions may have been bad, but not necessarily from a private perspective. “Heads I win, tails part of my losses are borne by taxpayers”. Of course I’d take more risk with those odds.

And yet despite this clear explanation of how moral hazard works, Matt Levine follows a description of how SVB went bankrupt with this head scratcher:

No! The fact that things didn’t work out for the executives doesn’t have any bearing on the question of whether moral hazard distorted decision-making at SVB.

The second misconception above also illustrates a basic lack of understanding of moral hazard. Yes, people don’t tend to pay attention to bank balance sheets when making decisions on where to put their money. But that’s exactly what you’d expect to happen if moral hazard were a major problem. People would stop caring about bank risk, and highly risky banks would understand that they could attract deposits every bit as easily as conservative, well-run banks. Clueless depositors are not evidence of a lack of moral hazard; they are evidence that moral hazard exists.

At this point people often shift their argument. They say, “Yes, it’s unfortunate that depositors don’t discipline banks, but you certainly cannot expect average people to evaluate the safety and soundness of large complex banks.” Really? Are these claims also true?

1. Most average people don’t read academic papers and attend lectures at lots of universities, hence you cannot possible expect average people to know that Harvard and Stanford are better that South Dakota State and Western Michigan University.

2. Most people are not able to evaluate the quality of carburetors, anti-lock brakes, and fuel injection mechanisms, so they couldn’t possibly be expected to know that a Mercedes is better than a Ford.

3. Most people are not able to evaluate the quality of surgeons, so they cannot possible be expected to know that Johns Hopkins is better than Missouri Valley Hospital.

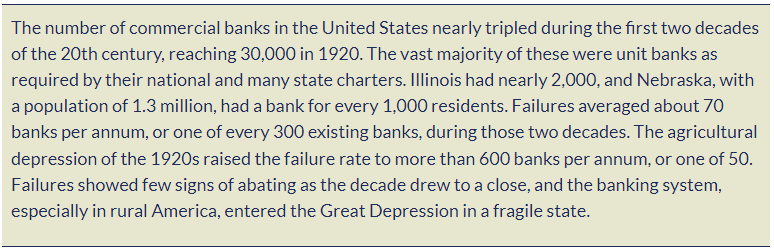

Yes, modern Americans pay little or no attention to the relative safety of various banks. Why should they? But I assure you that back in the 1920s people cared a great deal about bank safety. Banks knew this, and managed their balance sheets far more conservatively than do modern banks. That’s why big city banks used to look like massive Greek temples; they had to convince depositors that they had the capital to survive hard times. The vast majority of big banks survived the Great Depression. US GDP in 1929 was about $100 billion and deposit losses during the Great Depression were $1.3 billion. Today, a 50% fall in NGDP (as in 1929-33) would wipe out almost our entire banking system. Modern bankers are far more reckless “despite” regulation. The negative effects of deposit insurance are far more important than the positive effects of regulation.

When people think about moral hazard, they often exhibit a lack of imagination. If you read a great deal of history, you often find yourself asking, “How could people have behaved that way? What were they thinking?” Take an example from the 19th century. One aristocrat insults another at a well-attended dress ball. How would you react? Now think about how you would react if you had been born in 1820. You might respond to the rude comment with a challenge to a duel. Pistols at 20 paces, 6am the following morning. We can’t imagine living this way, because we never experienced this world.

A world without deposit insurance is not that far away. When I was 10 years old (1965), Canada had no deposit insurance and got along just fine. People who live in that sort of world know how to behave. They know enough to put their money in safe banks, not reckless banks. I wish Canada had never adopted deposit insurance. (I suppose their decision to do so represented the misguided big government liberalism of the late 1960s.)

Of course, the US system is much different from the Canadian system. Prior to FDIC, we had lots of bank failures. This was due to the almost incredibly undiversified nature of our system, which resulted from some pretty insane branch banking restrictions. Here’s Elmus Wicker:

LOL at Nebraska. Given the large size of families back then, that’s roughly one bank for every 250 families!

Contrary to widespread opinion, (even among many economists), the bank failures of this period did not lead to much contagion. The only real “panic” occurred for entirely different reasons, when there was (well-justified) fear that the US would leave the gold standard. Otherwise, lots of inefficient small banks failed and life went on.

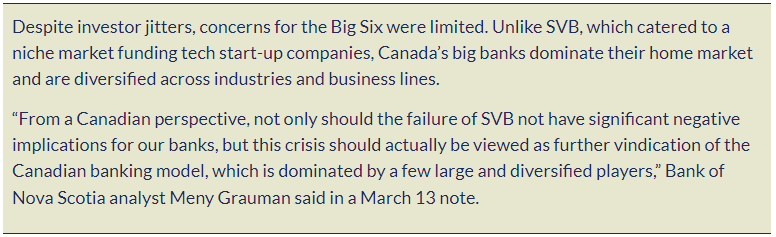

The Canadians were much smarter. They allowed large well-diversified banks, and thus have looked on with bemusement as the US reels through one banking crisis after another. Here’s the Financial Post:

In the US, both left and right wing politicians favor the smaller banks. Big is viewed as bad. Matt Yglesias is one of the few progressives that understands the value of big banks, and today he has an excellent post on the issue:

How do we get to Yglesias’s utopia? Abolish deposit insurance (he wouldn’t agree). You’ll see a massive shift of deposits toward the larger, more diversified banks, making our system resemble the Canadian system.

Most people, and even most economists, know nothing about our banking history. They’ve never bothered to read Elmus Wicker, Larry White, George Selgin, or any of the other experts. They get their ideas from films like “It’s a Wonderful Life.” They view our banking system as a fragile house of cards that would collapse without FDIC. (Funny how the Canadian house of cards avoided any major problems in the century before 1967.) Actually, it’s a house of cards created by FDIC.

The final misconception involves the effect of banking crises on the macroeconomy. It’s true that banking crises are often associated with recessions, but not always. Industrial production soared 57% between March and July 1933, despite many of America’s banks being shut down to check their balance sheets. In fact, in a fiat money system causality generally goes from the business cycle to banking distress, not the other way around. The US entered recession in December 2007. The recession got much worse after June 2008. The banking crisis occurred in late September 2008.

As long as the Fed adjusts monetary policy to keep expected NGDP growth at a healthy level, bank failures should have no significant impact on economic growth. In any case, creating moral hazard doesn’t prevent banking crises, it simply pushes the problem into the future.

FDR opposed deposit insurance, as he (correctly) feared it would create moral hazard. Unfortunately, Congress refused to listen to his good advice.

PS. Some other misconceptions:

“FDIC fees are not a tax on the public.” Yes, they are.

“We aren’t bailing out bank executives”. No, we are not bailing out SVB executives, but we are (implicitly) bailing out their competitors.

Original Article: https://www.econlib.org/the-wrong-way-to-think-about-moral-hazard/